Deciding to go solo sounds freeing until you sit down and realise you need a legal structure set up, a bank account that does not mix with groceries, a contract template you trust, and some way to send an invoice that actually gets paid. The scattered advice — half from YouTube, half from a blog last updated in 2019 — makes it hard to know where to start without spending weeks down rabbit holes. This article walks through the core things to prepare before you launch, in the order a solo business owner actually needs them, so you can move from ‘thinking about it’ to a working foundation in a few deliberate afternoons.

Key Summary: The Foundation You Cannot Skip

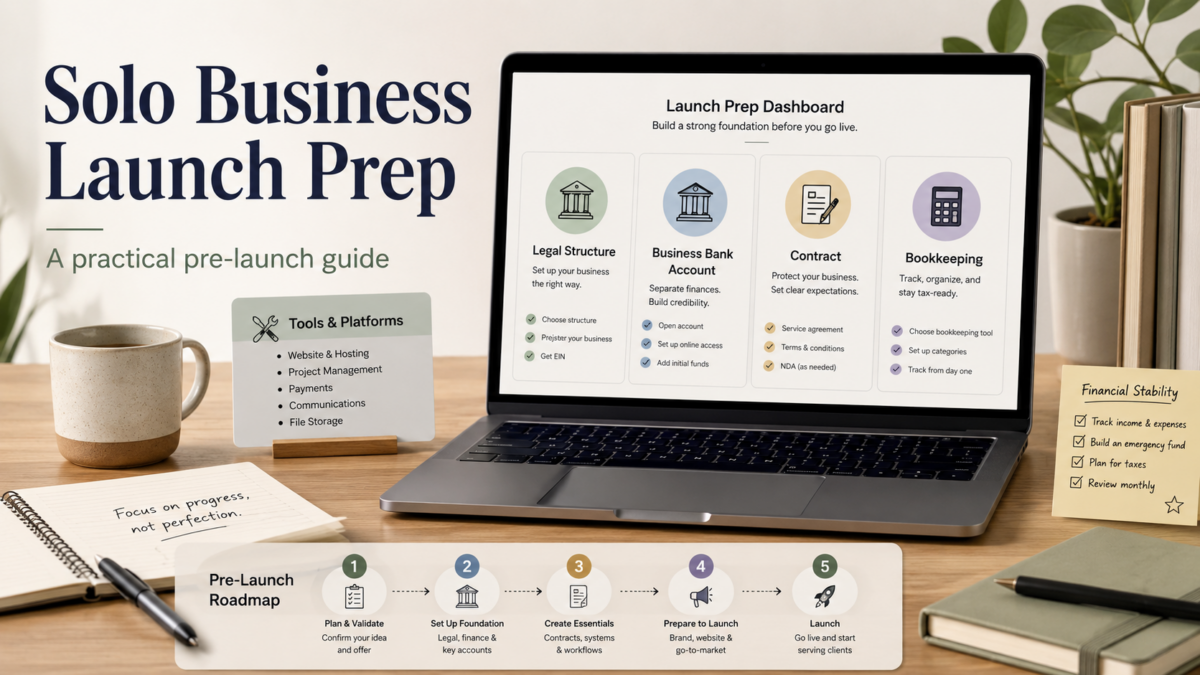

If I were setting this up myself, I would focus on four moves first: pick a legal structure (sole proprietorship or LLC), open a separate business bank account, create a simple contract that you can reuse, and set up a way to track income and expenses. These four decisions prevent most early-stage chaos — crossed money, misunderstandings with clients, and tax surprises. For a freelancer offering services, a sole proprietorship is faster and cheaper to start, but an LLC adds a layer of personal liability protection that is worth considering if your work carries risk. Check your state’s specific registration rules because the cost and paperwork vary more than most articles admit.

Beyond the legal and money side, keep your tool stack intentionally small at first. A basic invoicing app and a folder with your contract and client notes will take you further than a suite of 12 tools before you have a single paying client. The rest of this guide breaks each piece down so you can decide what fits your situation, not someone else’s checklist.

Why Setting Up Properly Matters Right Now

More people are turning to freelancing and solo businesses as full-time roles become harder to find or feel too rigid. Creative Lives In Progress notes that for many creatives, freelancing has shifted from a leap to a necessity. But alongside that shift comes a pile of admin — taxes, contracts, late payments — that solo owners often underestimate until it bites them. Setting up your business structure and systems early is not just about looking professional; it is about giving yourself a legal and financial container that keeps your personal assets separate when something goes wrong.

From a non-developer PM perspective, I treat this the same way I would treat setting up a new project repository: define the environment, lock down the permissions, and document how things run before you ship anything. If you wait until you have five clients to open a business bank account or figure out quarterly taxes, you are already untangling a mess. The cost of not doing this upfront is hidden time and stress you will pay later.

The Core Setup: Legal, Financial, and Operational Must-Haves

Every solo business sits on a handful of structural decisions. The Freelancer Startup Checklist from Freelance From Scratch and the Zenind guide for new solo entrepreneurs both emphasise that treating freelancing like a real business from day one means nailing the legal and financial foundation. Below are the items I would prioritise if I were preparing alone.

First, decide on a business structure. For most solo service providers, a sole proprietorship is the simplest path — no extra registration apart from a local business license in some areas — but it offers zero separation between business and personal liability. An LLC creates a legal wall but involves state filing fees, annual reports, and sometimes a registered agent. The choice usually comes down to how much risk your work carries and how much paperwork you can stomach in year one. Use the table below to weigh your options.

After your structure, open a dedicated business bank account, even for a sole proprietorship. This step alone makes tax time ten times easier and signals to clients that they are paying a business, not a person. Pair it with a simple bookkeeping tool like Wave (free) or a paid option that handles estimates and recurring invoices. Contracts are next — a reusable service agreement with scope, payment terms, and kill fees protects both sides. Templates are widely available; have a lawyer review yours once, then tweak for each project. Insurance is the final layer many solo owners skip until they need it: general liability for premises risk and professional liability (errors and omissions) if you give advice or build things for clients.

| Consideration | Sole Proprietorship | LLC |

|---|---|---|

| Ease of Setup | Minimal — may only need a local DBA | State filing required, plus possible publication or annual fees |

| Personal Liability Protection | None — you are the business | Separates business and personal assets in most cases |

| Tax Filing | Reported on your personal return (Schedule C) | Still pass-through for single-member, but more formal records needed |

| Best For | Low-risk service work early on | Contracts with higher liability, or if you expect to scale |

- Open a separate business checking account (free online options exist; compare fee structures).

- Choose one bookkeeping tool (Wave, Bonsai, or FreshBooks) and connect it to your bank feed.

- Draft a contract template and have it reviewed once by a legal professional.

- Get a simple invoicing flow — many tools combine books, contracts, and invoices.

- Research professional liability insurance if your work includes consulting, development, or creative deliverables.

Step‑by‑Step: Laying Your Solo Business Foundation This Week

For a solo business owner, I would not try to do everything at once. The following ordered list uses a hypothetical, early‑stage freelance consultant as the base case, but the sequence works for most service‑based solo founders. Each step moves you from zero to an operational setup that can accept a client payment safely.

- Define your service and a single clear offer

Write down exactly what you do and for whom, in one sentence. For example, ‘I help local retail businesses set up their Google Business Profile and manage reviews.’ This clarity makes every later step — from legal structure to marketing — faster. If you cannot describe it in one breath, narrow it down before spending money on registration. - Register your business name and structure

Go to your state’s Secretary of State website and search for an LLC filing or a DBA (‘doing business as’) if you use a trade name. Most states allow online filing. Grab any required local business license at the same time; the requirements are usually on your city’s website. Save all confirmation documents in a folder called ‘Legal’ — you will need them for the bank account. - Get an EIN and open a business bank account

Apply for an Employer Identification Number directly on the IRS website; it is free and instant. With that EIN and your business registration, open a separate checking account. If I were setting this up myself, I would look at online banks with no monthly fees and built‑in bookkeeping integrations to avoid extra transfer steps. - Set up a combined invoicing and bookkeeping tool

Pick one tool that handles estimates, invoices, and expense tracking (Wave, Bonsai, or another aimed at freelancers). Connect your new bank account to auto‑import transactions. Create your first invoice template with your business name, payment terms, and a note about late fees. Send a test invoice to your personal email to see how the client experience feels. - Draft a contract and get it reviewed

Start with a reputable template — many freelance platforms and lawyer‑reviewed sites offer them. Customise the scope, payment schedule, revision limits, and termination clause. Spend the few hundred dollars to have a local small‑business lawyer review it once, then keep it as your base for every project. Never start work without a signed version, even for a friend. - Assess insurance need and get a quote

If you visit client sites, handle data, or produce deliverables where mistakes matter, talk to an insurance broker or use an online comparison tool for general and professional liability. Start with the minimum coverage your contracts might require. For many early-stage freelancers, you may delay this if you have low risk, but at least know the trigger point that would push you to buy it.

Matching the Setup to Your Solo Business Type

Not every solo business is the same. A freelance writer, a part‑time IT consultant, and a small local service business have different exposure and tool needs. The table below shows where I would put my first energy depending on the type. Use it as a filter, not a prescription, because your location, existing client list, and risk tolerance shift the priorities.

For a freelancer offering creative or consulting services, for example, time‑tracking and a polished contract matter more than a business website. For a solo founder building a product or an online course, intellectual property terms and a platform that handles payments and taxes become critical. The SCU home‑based business readiness checklist reinforces that starting lean is normal — some businesses need only a laptop and a flyer, but you still need a system to track income and legal protection.

| Solo Business Type | First Priority to Lock Down | Recommended Approach |

|---|---|---|

| Freelance services (writing, design, dev) | Solid contract + invoicing flow | Use a template, get it reviewed, and send it with every proposal. Pick a tool that handles recurring invoices. |

| Consulting and coaching | Professional advice boundary + insurance | Check if your advice could be considered professional liability; error‑and‑omissions insurance might be a must. |

| Local hands‑on service (photography, repair) | General liability insurance + local permits | Many venues or clients require proof of insurance before you show up. Handle this early. |

| Product or digital‑product business | Terms of service, return policy, and payment processor | Platforms handle some of this, but cross‑check your liability and refund obligations yourself. |

Pre‑Launch Checklist and Pitfalls to Avoid

If I were preparing alone on a tight timeline, I would run through the items below in the week before my first client payment lands. They are meant to catch the problems that cause the most regret in early solo stories.

It is tempting to skip the less exciting steps — getting a separate bank account, actually writing down your payment terms, setting quarterly tax reminders — because they feel like overhead with no immediate return. But from everything I have read, those are exactly the steps that separate a business that can survive a rough month from one that quietly collapses under admin and surprise bills.

- Open a business checking account and do not use it for personal spending.

- Save 25–30% of every incoming payment in a separate tax reserve account.

- Have a signed contract or at least a written statement of work before starting any project.

- Set up quarterly estimated tax reminders on your calendar (US: March, June, September, January).

- Keep all business receipts in one place — a folder, an app, or a dedicated credit card.

- Back up client files and communication in a place you control, not just inside a platform.

- Test your invoicing tool with a real‑looking sample and check how the payment link works on mobile.

|

💡 Common Pitfall |

|

💡 Tool Trap Warning |

Frequently Asked Questions

Do I need an LLC right away, or is a sole proprietorship enough to start?

For many service‑based freelancers, a sole proprietorship is the fastest and cheapest way to begin. You report income on your personal tax return and avoid state filing fees. The trade‑off is that your personal assets are not separated from the business. If your work carries higher liability (consulting, development, handling sensitive data), forming an LLC early can protect you. Check your state’s rules and the nature of your first few clients to decide.

How much money should I save before leaving my job to start a solo business?

There is no single figure, but N26’s freelancing guide suggests treating financial stability as a key signal. A common rule of thumb found in practical guides is to have 3–6 months of living expenses set aside, plus a buffer for business startup costs (registration, insurance, tools). Starting part‑time while employed lowers the pressure and lets you test the market before relying on solo income.

What are the absolute essential tools I should pay for on day one?

Start with a bookkeeping and invoicing tool that connects to your bank account (for example, Wave or FreshBooks). A domain name for a simple portfolio site or email address is also worth the small cost. Hold off on project management suites, marketing software, and complex automation until you have a steady workflow. The Freelance From Scratch checklist breaks down tool categories but notes you do not need them all at once.

How do I handle taxes when I am the only person in the business?

In the US, sole proprietors and single‑member LLCs generally report business income on Schedule C of their personal tax return and pay self‑employment tax. You should make quarterly estimated tax payments to avoid penalties. The IRS provides a free EIN application online, and many bookkeeping tools generate the reports you need. Because tax rules change and vary by location, confirm requirements with your state’s department of revenue or a local accountant.

When should I get business insurance as a freelancer?

If a single mistake could create a significant financial loss for a client — think bad advice, buggy software, or property damage on site — professional liability (errors and omissions) and general liability insurance become important early. Some clients require proof before signing a contract. Start with a quote from a broker and compare it against the value of your contracts; if the cost of a potential claim far exceeds the premium, it is worth having before you start that kind of work.

Wrap-Up

Preparing for a solo business is less about having everything perfect and more about creating a container that keeps mistakes contained and recoverable. Right now, the best next actions are to pick your legal structure, open a separate bank account, and get a contract template reviewed. From there, focus on landing one client while your systems are still simple — you can always add automation and fancier tools once you know what repetitive work actually drains your time.